INTRODUCTION

On March 11, 2020, the World Health Organisation declared COVID-19 as a pandemic. The pandemic remains amongst the most scathing times in living memory. Over a year into the pandemic, there continues to be loss of lives and livelihoods. According to the International Monetary Fund (IMF), an additional 95 million people have fallen below the threshold of extreme poverty in 2020, reversing a two-decade trend of global poverty reduction. Several countries have witnessed second and third wave eruptions of the virus, necessitating intermittent restrictions and lockdowns. COVID-19 has accelerated the speed of adoption of digital technologies across all spheres of activity and these positive changes are likely to be long sustaining trends. While new variants and mutating viruses remain a challenge, the rapid roll-out of vaccines across the globe has given rise to some degree of optimism in overcoming the pandemic. In April 2021, India’s second wave of infections increased significantly in its intensity.

Global Macroeconomic Overview

Despite disruptions and prevailing uncertainties, the global economic outlook continued to improve. After a global economic contraction of 3.3% in calendar year 2020, the IMF is projecting global growth to recover to 6% in calendar year 2021. This is based on continued fiscal stimulus measures, accommodative monetary policies and a wider coverage of a vaccinated population. The stronger than anticipated recovery is also attributed to resilience and quick adaptation to life during a pandemic. Communication and technology tools have enabled several businesses to ensure business continuity, despite extant challenges. Yet, divergent recovery paths have resulted in widening inequalities, particularly for contact-intensive sectors, the marginalised and low skilled workers.

Indian Macroeconomic Overview

From March 25, 2020 till June 8, 2020 India was under a severe lockdown. The suddenness of the announcement triggered widespread concerns as all activities, barring few essential services were mandated to close. This led to massive supply disruptions and demand destruction. Income losses and unemployment scaled levels never seen before. In the early part of FY21, an exodus of migrant workers faced acute hardships as they attempted to leave the cities they worked in and return to their villages. As a result of the strict lockdown, the first quarter of FY21 resulted in a GDP contraction of 24.4%.

During the second quarter of FY21, as lockdown restrictions gradually eased, high frequency indicators such as goods and services tax collections, e-tolls, auto sales, railway freight, electricity consumption, amongst several others began exhibiting signs of recovery. The economy recuperated with GDP growth contracting by 7.3% in the second quarter and recording a positive growth rate of 0.4% in the third quarter of FY21.

As per advance estimates by the National Statistical Office, India’s GDP is expected to contract by 8.0% in FY21. Notwithstanding uncertainties on the extent of recurrent waves of infections, the Indian economy is expected to be on a recovery trend. In April 2021, the Reserve Bank of India (RBI) had projected GDP growth for FY22 at 10.5%.

Other macro fundamentals of the Indian economy continued to remain strong. Total foreign portfolio investment inflows in debt and equity stood at USD 37 billion in FY21. Foreign exchange reserves stood at USD 577 billion as at March 31, 2021. India now holds the fourth largest foreign exchange reserves in the world.

As at March 31, 2021, year-on-year bank deposit growth grew by 11.4%, however, bank credit growth remained subdued at 5.6% despite sharp reductions in interest rates, reflecting a continued risk averse environment.

In April 2021, India witnessed an eruption of a second wave of infections. This resurgence has placed immense strain on the healthcare infrastructure of the country. Yet, India holds 60% of the global vaccine manufacturing capacity and there remains hope of a speedy roll-out of vaccinating its vast population. As of date, unlike in the previous wave of infections, there is no national lockdown stipulated by the central government. Instead, the strategy of micro-containment zones has been adopted and various state governments have announced lockdowns or restrictions of varying degrees. At this juncture, there remains a great deal of uncertainty on the impact the second wave would have on the Indian economy.

Housing and Real Estate Markets

The demand for housing remained strong during the year. Low interest rates, softer or stable property prices, improved affordability, continued support of fiscal incentives on a home loan and concessional stamp duty rates offered by certain states were factors that encouraged more homebuyers. The housing market was buoyant with an increased number of first-time homebuyers and buyers opting for larger homes or acquiring homes in another location. Given the low mortgage to GDP penetration at 10% in India and the continued shortage of housing, it is evident that the demand for housing is structural and not pent up demand.

Segments of the real estate sector continued to face stress. Construction activity came to a complete halt in March 2020 with the announcement of the nationwide lockdown. Though by June 2020, restrictions were gradually lifted, construction activities did not resume especially in the major metro cities as there remained a paucity of labour. Following the end of the monsoon season, from September 2020 onwards, activity on construction sites resumed.

Developers who were overleveraged in the pre-pandemic period were more severely impacted by the pandemic. Given the prevailing conditions, many developers were willing to negotiate in order to swiftly close out property deals. This helped reduce unsold inventories and improve overall cash flows. Some developers increased their equity, entered into joint development agreements, availed of last mile funding or monetised their non-core assets to improve their financial positions.

The demand for data centres and warehousing increased, while sectors like retail and malls were impacted by the pandemic.

During the year, the government announced various measures to help the real estate sector. Some of these were:

INTEREST RATES AND LIQUIDITY SCENARIO

In the initial months of the financial year, liquidity remained extremely tight. Given the uncertainties due to COVID-19, credit markets turned very risk averse. However, with the steady interventions by RBI through large infusions of liquidity, interest rates steadily declined. In March 2020, RBI reduced the repo rate by 75 basis points (bps) and in May 2020 it reduced the rate by another 40 bps, thus aggregating an overall reduction of 115 bps.

Market rates began to inch up in the fourth quarter of FY21 against the backdrop of concerns on rising infections, sharp rise in US treasury yields and due to the announcement of the government’s large borrowing programme for FY22, estimated at ` 12 lac crore. RBI once again intervened through various monetary tools and reiterated its commitment towards an accommodative monetary policy stance to support growth and ensure an orderly evolution of the yield curve. This helped to quell market concerns.

Overall, the total liquidity support announced by RBI since February 6, 2020 up to March 31, 2021, amounted to ` 13.6 lac crore. This entailed a combination of open market operations, variable rate repos, long-term repo operations, targeted long-term repo operations (TLTRO 1.0 and 2.0), reduction in the cash reserve ratio and statutory liquidity ratio of banks, special liquidity facility for mutual funds, refinance lines to NABARD, SIDBI, NHB and Exim Bank and simultaneous purchase and sale of securities under special open market operations to better manage the yield curve. The banking system remained in surplus throughout FY21 and the surplus ranged between ` 2.1 lac crore and ` 6.7 lac crore.

During the year, there was a significant improvement in monetary transmission to deposit and lending rates of banks. According to RBI, the weighted average lending rate on fresh rupee loans declined by 107 bps since March 2020, in response to the reduction of 115 bps in the policy repo rate.

IMPACT OF COVID-19

The Corporation identified three pillars as key monitorables to assess the financial impact of COVID-19 on the Corporation:

The Corporation was able to raise resources from multiple sources. The Corporation stands comfortable on liquidity.

During the year, the risk averse environment continued for non-individual loans and the Corporation opted to restrict its lending to select, high rated entities.

On an overall basis, the Corporation is well geared towards being able to serve its customers through its digital platforms and/or its physical offices.

SIGNIFICANT CHANGES IN THE REGULATORY FRAMEWORK

On February 17, 2021, RBI issued Master Direction - Non-Banking Financial Company - Housing Finance Company (Reserve Bank) Directions, 2021. These directions came into force with immediate effect.

Some of the significant changes include the change in the definition of ‘principal business’ and ‘housing finance’. Accordingly, a company will be treated as a Non-Banking Financial Company – Housing Finance Company (NBFC-HFC) if it meets two key conditions. First, of the total assets (netted off by intangible assets), not less than 60% should be towards providing finance for housing. Second, out of the total assets (netted off by intangible assets), not less than 50% should be by way of housing finance for individuals.

RBI has also stipulated specific criteria as to what comprises housing finance. Accordingly, the Corporation’s overall portfolio mix of housing and non-housing loans will undergo a change as per the new regulations.

A timeline for transition has been provided by RBI as follows:

| Timeline | Minimum percentage of total assets towards housing finance | Minimum percentage of total assets towards housing finance for individuals |

|---|---|---|

| March 31, 2022 | 50% | 40% |

| March 31, 2023 | 55% | 45% |

| March 31, 2024 | 60% | 50% |

As per the directions, the Corporation has submitted a board approved plan to RBI indicating timelines for the transition.

Another significant change in the directions entail Guidelines on Liquidity Coverage Ratio (LCR). NBFC-HFCs are required to maintain liquidity buffers to withstand potential liquidity disruptions by ensuring that it has sufficient High Quality Liquid Assets (HQLA) to survive any acute liquidity stress scenario lasting for 30 days. As per the guidelines, the weighted values of the net cash flows are calculated after the application of respective haircuts for HQLA and considering stress factors on inflows at 75% and outflows at 115%.

For all deposit taking NBFC-HFCs, there is a phased transition towards meeting the minimum LCR as given below:

| From | December 01, 2021 | December 01, 2022 | December 01, 2023 | December 01, 2024 | December 01, 2025 |

|---|---|---|---|---|---|

| Minimum LCR | 50% | 60% | 70% | 85% | 100% |

The Corporation has put in place a liquidity risk management framework so as to adhere to the above-mentioned guidelines and timelines.

COVID-19: KEY REGULATORY FORBEARANCES & SCHEMES

To alleviate COVID-19 induced financial stress various measures, forbearances and schemes were put in place by the government, RBI and other authorities. Some of these include:

The validity of ECLGS 1.0 and 2.0 is up to June 30, 2021 and or till guarantees of an aggregate amount of ` 3 lac crore is reached. Disbursements have to be availed before September 30, 2021.

FINANCIAL AND OPERATIONAL PERFORMANCE

Financial Performance

Total income of the Corporation for the year ended March 31, 2021 was ` 48,176 crore.

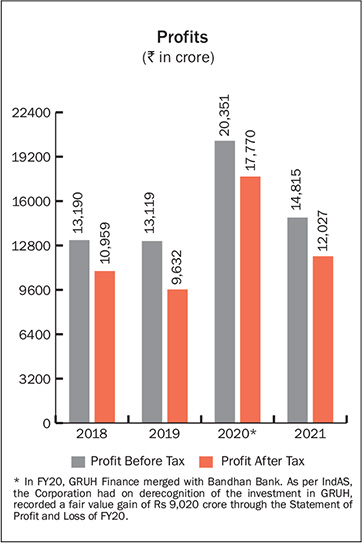

The financials for the year ended March 31, 2021 are not comparable with that of the previous year. In the previous year, the Corporation had fair value gain consequent to the merger of GRUH Finance Limited (GRUH) with Bandhan Bank Limited amounting to ` 9,020 crore. The total income in the previous year was ` 58,763 crore. Further, during the year, profit on sale of investments and dividend income was lower compared to the previous year.

Total expenses stood at ` 33,361 crore compared to ` 38,412 crore in the previous year. Partly owing to the low interest rate regime during the year under review, the lower revenue from operations was offset by reduced expenses as well.

The net interest income (NII) for the year ended March 31, 2021 stood at ` 15,172 crore compared to ` 12,904 crore in the previous year, representing a growth of 18%. Inclusive of fees and income on assigned loans, the NII for the year ended March 31, 2021 stood at ` 16,372 crore compare to ` 13,909 crore in the previous year.

The reported profit before tax for the year ended March 31, 2021 stood at ` 14,815 crore compared to ` 20,351 crore in the previous year.

After providing for tax of ` 2,788 crore (Previous Year: ` 2,581 crore), the profit after tax before other comprehensive income for the year ended March 31, 2021 stood at ` 12,027 crore compared to ` 17,770 crore in the previous year.

To reiterate, the reported profit numbers for the year are not comparable with those of the previous year owing to the following:

To facilitate a like-for-like comparison, after adjusting for profit on sale of investment, fair value gain consequent to the scheme of amalgamation, other fair value changes, income of loans assigned, dividend, employee stock options and provisioning, the adjusted profit before tax for the year ended March 31, 2021 is ` 13,823 crore compared to ` 11,586 crore in the previous year, reflecting a growth of 19%.

The total comprehensive income for the year ended March 31, 2021 stood at ` 13,762 crore compared to ` 11,117 crore in the previous year.

Statement of Profit and Loss

Key elements of the statement of profit and loss for the year ended March 31, 2021 are:

Spread on Loans

The average yield on loan assets during the year was 8.99% per annum compared to 10.18% in the previous year. The average all-inclusive cost of funds was 6.70% per annum as compared to 7.91% in the previous year. The spread on loans over the cost of borrowings for the year was 2.29% per annum as against 2.27% in the previous year. Spread on individual loans for the year was 1.93% and on non-individual loans was 3.22%.

Operational Performance

Lending Operations

Despite the challenges posed by the pandemic, lending operations of the Corporation continued seamlessly during the year. Much of this was attributed to the ability to stay connected with customers by leveraging on the Corporation’s digital platforms.

Individual loan business was impacted in the first quarter of the financial year owing to the strict national lockdown imposed. However, as restrictions gradually eased, the individual loan business saw month-on-month improvements.

The individual loan business began to see normalcy return from the month of September 2020 onwards. In the second half of the financial year, the demand for housing remained robust, with growth trends exceeding expectations. Growth in home loans was aided by low interest rates, softer or stable property prices, continued fiscal benefits on home loans and concessional stamp duty rates offered in certain states.

Individual disbursements in the first half of the financial year was 35% lower compared to the corresponding period in the previous year. In the second half of the financial year, individual disbursements were 42% higher compared to the corresponding period in the previous year. Consequently, during the year ended March 31, 2021, individual loan disbursements reported a growth of 3% compared to the previous year.

The average size of individual loans stood at ` 29.5 lac during the year, compared to ` 27.0 lac in the previous year. The increase in the average loan size is largely attributable to the fact that demand for home loans was from both, affordable housing and higher end properties.

Based on loans disbursed during the year, 78% were salaried customers, while 22% were self-employed (including professionals). In terms of the acquisition mode, of the loans disbursed during the year, 55% were first-purchase homes i.e. directly from the builder, 37% were through resale and 8% self-construction.

As at March 31, 2021, cumulatively, the Corporation had financed 8.4 million housing units.

Affordable Housing

The Corporation continued its commitment towards supporting the government’s flagship scheme, ‘Housing for All’ and pursued efforts towards lending to the Economically Weaker Section (EWS), Low Income Group (LIG) and Middle Income Group (MIG) segments.

The Corporation has the largest number of home loan customers – of approximately 2.3 lac who have availed benefits under the Credit Linked Subsidy Scheme (CLSS). As at March 31, 2021, cumulative loans disbursed by the Corporation under CLSS stood at ` 39,333 crore and the cumulative subsidy amount stood at ` 5,211 crore.

The Corporation continued its focus on lending to credit worthy home loan customers across all income segments as reflected in the table below.

Housing Loan Approvals to Customers Based on Income Slabs in FY21

| Category | Household Income per annum | Home Loan Approvals in

FY21 |

|

|---|---|---|---|

| % in Value Terms | % in Number Terms | ||

| Economically Weaker Section | Up to ` 3 lac | 2% | 6% |

| Low Income Group | Above ` 3 lac up to ` 6 lac | 14% | 27% |

| Middle Income Group | Above ` 6 lac up to ` 18 lac | 44% | 48% |

| High Income Group | Above ` 18 lac | 40% | 19% |

| Total | 100% | 100% | |

The average home loan to the EWS and LIG segment during the year stood at ` 10.8 lac and ` 18.6 lac respectively.

Rural Housing

Against the backdrop of a good monsoon and strong agricultural growth, the rural economy remained buoyant. The Corporation continued its focus on rural housing, providing loans to both, salaried and selfemployed customers for properties situated in rural areas. Most of these customers have household incomes from agriculture and agriallied industries. The properties under rural housing are located either in the hinterland or in peripheral areas closer to larger cities. Rural housing loans accounted for approximately 9% of individual loans disbursed during the year.

Non-Individual Loans

As far as non-individual loans were concerned, the Corporation opted to be cautious in lending, given the continued risk averseness. Several developers remained under stress and construction activity of on-going projects did not resume till the second quarter of the financial year which is when the labour force began to return back to the construction sites. The Corporation remained selective in incremental lending for construction finance given the prevailing stress in the sector.

The Corporation, however, supported efforts of the government and RBI to help alleviate COVID-19 induced stress by extending loans to eligible borrowers under ECLGS and facilitating the one-time restructuring scheme.

During the year, the Corporation focused on lending to select, top grade corporates.

As a result of the development of the real estate investment trust (REITS) market in India, the Corporation received large prepayments on its lease rental discounting book which was also one of the reasons why the non-individual loan book showed a lower growth.

Loan Portfolio

The loan approval process of the Corporation is decentralised, with varying approval limits. The Corporation has a three-tiered committee of management structure with varying approval limits. Larger proposals, as appropriate, are referred to the Board of Directors.

The Assets Under Management (AUM) as at March 31, 2021 amounted to ` 5,69,894 crore as compared to ` 5,16,773 crore in the previous year.

On an AUM basis, the growth in the individual loan book was 12% and the non-individual loan book was 4%. The growth in the total loan book on an AUM basis was 10%.

During the year, the Corporation’s loan book increased from ` 4,50,903 crore to ` 4,98,298 crore as at March 31, 2021. In addition, total loans securitised and/or assigned by the Corporation and outstanding as at March 31, 2021 amounted to ` 71,596 crore.

The table below provides a synopsis of the gross loan book of the Corporation:

(` crore)

| As at March 31, 2021 |

As at March 31, 2020 |

|

|---|---|---|

| Individual Loans | 3,68,804 | 3,25,923 |

| Corporate Bodies | 1,22,707 | 1,18,165 |

| Others | 6,787 | 6,815 |

| Total | 4,98,298 | 4,50,903 |

The net increase in the loan book during the year, (after removing the loans that were sold) stood at ` 47,395 crore.

Principal loan repayments stood at ` 92,111 crore compared to ` 90,223 crore in the previous year after excluding loans written off during the year amounting to ` 1,372 crore (Previous Year: ` 995 crore).

Prepayments on retail loans stood at 10.3% of the opening balance of individual loans compared to 10.9% in the previous year. 64% of these prepayments were full prepayments.

Of the total loan book (including loans sold), individual loans comprise 77%.

The growth in the individual loan book, after adding back loans sold in the preceding twelve months was 19% (13% net of loans sold).

Non-individual loans grew by 4% during the year and comprised 23% of the portfolio.

The growth in the total loan book would have been 15% had the Corporation not sold any loans during the year.

Assignment/Sale of Loans

During the year, the Corporation, sold individual loans amounting to ` 18,980 crore (Previous Year: ` 24,127 crore). All the loans assigned during the year were to HDFC Bank pursuant to the buyback option embedded in the home loan arrangement between the Corporation and HDFC Bank. Of the total loans sold during the year, ` 5,671 crore qualified as priority sector advances for banks.

As at March 31, 2021, individual loans outstanding in respect of all loans assigned/securitised stood at ` 71,421 crore. HDFC continues to service these loans.

The advantage for the Corporation in selling loans under the loan assignment route is that there is no credit enhancement to be provided by the Corporation on the loans sold and the credit risk is passed on to the purchaser. The assignment of loans is also Return on Equity accretive to the Corporation as no capital or provisioning is required to be maintained on these loans.

Product-wise Loan Performance

As at March 31, 2021, the productwise break-up of loans on an AUM basis was -- individual loans: 77%, corporate loans: 6%, construction finance: 10% and commercial lease rental discounting: 7%.

During the year, on an AUM basis, 92% of the incremental growth in the loan book came from individual loans and 8% from non-individual loans.

Sourcing of Loans

The Corporation’s distribution channels which include HDFC Sales Private Limited (HSPL), HDFC Bank and third party direct selling associates (DSAs) play an important role in sourcing home loans.

HDFC has third party distribution tieups with commercial banks, small finance banks, non-banking financial companies and other distribution companies including e-portals for retail loans. All distribution channels only source loans, while the control over the credit, legal and technical appraisal continues to rest with HDFC, thereby ensuring that the quality of loans disbursed is not compromised in any way and is consistent across all distribution channels.

In value terms, HSPL, HDFC Bank and third party DSAs sourced 54%, 27% and 17% of home loans disbursed respectively during the year. 83% of the Corporation’s individual loan business during the year was sourced directly or through the Corporation’s affiliates.

Physical and Digital Reach

Geographic Reach

The Corporation’s physical distribution network now spans 593 outlets, which includes 203 offices of HDFC’s wholly owned distribution company, HSPL. During the year, efforts were focused on expanding into deep geographies so as to widen the Corporation’s footprint. These outlets are typically manned by one or two individuals and leverage completely on the digital platforms of the Corporation.

HDFC has overseas offices in London, Singapore and Dubai. The Dubai office caters to customers across Middle-East through its service associates.

Digitalisation Initiatives

While the Corporation already had several digitalisation tools and platforms in place to support the lending business, the suddenness of shifting to remote working owing to the COVID-19 outbreak hastened the pace and adoption of digital infrastructure for a number of products and services. For instance, the digital on-boarding platform, which was used for direct and website based applications was opened up for all channel partners. The Corporation’s mobile app for channel partners facilitates real time tracking and processing of loan applications.

Direct fetch information from public portals like the Goods and Services Tax Network, Ministry of Corporate Affairs, Income Tax and tools like bank statement information analysers which provides real-time analytical capabilities are integrated into the loan processes, thereby strengthening loan origination and processing controls. Several other loan control checks have been automated. The application programming interface (API) has been facilitated through various fintech platforms.

During the year, approximately 81% of borrowers were digitally on-boarded. The Corporation has also piloted an end-to-end digitally enabled product, wherein all checks and controls are entirely system driven and loans are auto approved.

Digital platforms not only enabled business continuity during the lockdown, but has also helped process larger volumes with greater speed and efficiency. The Corporation has adopted a ‘One HDFC’ strategy which capitalises on using technology seamlessly and facilitates redeployment of manpower wherever it is most required. Thus, if there is a particular geography where there is an increase in business volumes, the Corporation optimises its use of resources so as to ensure that high customer service standards are maintained. Customers have responded well to the Corporation’s online platforms and have appreciated the ease of using such platforms.

Co-lending Arrangements

In an endeavour to broad base the Corporation’s reach, efforts were made towards entering into strategic co-lending partnerships for housing loans. Such arrangements entail the sharing of risk and reward on mutually agreed terms between colending partners.

The objective of the Corporation in entering into any co-lending arrangement is to tap into a wider customer base across different geographies. The advantage for a customer is that he/she gets a blended rate of interest on the loan.

The Corporation has ensured that all loans under such arrangements will be processed in accordance with standard operating procedures and as per the loan eligibility criteria as specified by the Corporation. Under this arrangement, there will be no change in the methodology of appraisal norms by the Corporation. Thus, the Corporation will retain all controls on appraisals of such loans.

Marketing Initiatives

During the year, the Corporation undertook a myriad of marketing initiatives whilst capitalising on digital platforms. The Corporation enhanced its automated chatbot service to enable its existing and new customers to connect and interact with the HDFC brand and get immediate, personalised service 24x7.

Recognising a growing preference towards voice assistance, the Corporation offers not only text based solutions, but voice based conversational solutions as well through popular voice activated smart devices. The Corporation is also driving ad campaigns, content strategies and digital campaigns on voice search.

To cater to those using local language searches, the Corporation serves ads and content on search engines in vernacular languages to be relevant to users looking for home loan related information in their regional language.

During the year, the Corporation’s aired four advertisement films based on the catchphrase, ‘the new normal’. The Corporation leveraged the surge in over-the-top (OTT) viewership and advertised the commercials on OTT channels as well. This allowed the brand to gain viewership of younger, engaged and varying audience profiles. The Corporation also strengthened its social media marketing on various platforms so as to reach out to a diverse audience group and deepen the brand engagement.

Leveraging its long-standing relationships with reputed developers from across the country, the Corporation organised virtual property exhibitions as a value-added service for home seekers, enabling them to shortlist, compare and choose from a wide range of property options.

As regards customer lifecycle management, the Corporation continued to focus on business growth by upselling and cross-selling products to existing customers at predefined milestones as guided by digital analytics.

Data Analytics

During the year, the Corporation capitalised on machine learning and artificial intelligence tools used in data analytics to provide insights for business growth, risk management and improve process efficiencies. Predictive and prescriptive models across the life cycle of the retail loans customer like acquisition, underwriting, delinquency, retention, amongst others are being built to support various business functions across the organisation. Through a unified data layer, efforts are being made to facilitate a 360-degree view of behaviour across the customer life cycle. The objective is to help better manage customer expectations.

Investments

The Investment Committee constituted by the Board of Directors is responsible for approving investment proposals in line with the limits as set out by the Board of Directors.

The investment function supports the core business of housing finance. The investment mandate includes ensuring adequate levels of liquidity to support core business requirements, maintaining a high degree of safety and optimising the level of returns, consistent with acceptable levels of risk.

As at March 31, 2021, the investment portfolio stood at ` 68,637 crore compared to ` 64,944 crore in the previous year. The proportion of investments to total assets was 12%. The increase in the investment portfolio during the year was primarily on account of the larger amounts invested in high quality liquid assets.

The Corporation maintained substantially higher liquidity buffers, owing to increased uncertainties and risk averseness in the financial sector. Accordingly, the average balances maintained in liquid mutual funds was significantly higher, especially in the first half of the year compared to the previous year.

NBFC-HFCs are required to maintain a statutory liquidity ratio (SLR) in respect of public deposits raised. As at March 31, 2021, the SLR requirement was 13% of public deposits.

As at March 31, 2021, the total government securities stood at ` 22,567 crore of which ` 13,816 crore was towards SLR and ` 8,751 crore comprised securities held towards liquidity support.

Surplus from deployment of liquid funds in cash management schemes of mutual funds was ` 813 crore.

The average yield on the non-equity treasury portfolio for the year was 5.2% per annum on an annualised basis.

Dividend received during the year was ` 734 crore, of which ` 717 crore was received from subsidiary companies.

As at March 31, 2021, the market value of listed equity investments in subsidiary and associate companies was higher by ` 2,61,590 crore compared to the value at which these investments are reflected in the balance sheet. This unaccounted gain includes appreciation in the market value of investments in HDFC Bank held by the Corporation’s wholly owned subsidiaries, HDFC Investments Limited and HDFC Holdings Limited. It, however, excludes the unrealised gains on unlisted subsidiaries such as HDFC ERGO General Insurance Company Limited, HDFC Credila Financial Services Limited, amongst others.

Asset Quality

Non-Performing Assets & Provisioning

Collection efficiency ratios for individual loans have improved, nearing pre-COVID levels. The collection efficiency for individual loans in March 2021 stood at 98.0% compared to 96.3% in September 2020.

In accordance with regulatory norms, gross non-performing loans outstanding amounted to ` 9,759 crore as at March 31, 2021, constituting 1.98% of the loan portfolio. The principal outstanding in respect of individual loans where the instalments were in arrears constituted 0.99% of the individual portfolio and the corresponding figure was 4.77% in respect of the nonindividual portfolio. During the year, certain cases in non-individual loans were resolved.

As per the prudential norms prescribed by RBI, the Corporation is required to carry a provision of ` 5,491 crore, of which ` 3,102 crore is on account of non-performing assets and the balance is in respect of standard loans. The regulatory provisioning for non-performing loans is determined solely on the period of default. The actual provisions carried as at March 31, 2021 stood at ` 13,025 crore.

Cumulative COVID-19 provision as at March 31, 2021 stood at ` 844 crore.

On a gross basis, the Corporation has written off loans aggregating to ` 1,372 crore during the year. On loans that have been written off, the Corporation will continue making efforts to recover the money. The Corporation has, since inception, written off loans (net of subsequent recovery) aggregating to ` 3,366 crore. Thus, as at March 31, 2021, the total loan write offs stood at 21 basis points of cumulative disbursements since inception of the Corporation.

In accordance with the write off policy of the Corporation, loans may entail either a partial or a full write off, determined on a case-by-case basis.

During the year, where recovery has proven to be difficult, the Corporation continued to adopt various methods to settle loans. The Corporation has also opted to reach settlements through sell-downs to asset reconstruction companies, institutions or private equity players. In certain overdue loans, the Corporation has resorted to the invocation of pledged shares.

The Corporation has in select cases, entered into debt asset swap arrangements entailing immovable property. Whilst entering into such arrangements, the Corporation’s key considerations are the marketability and saleability of the property, its present and expected valuation, demand and supply factors based on the location of the property, legal titles, whether it is free from encumbrances, amongst other factors. The properties taken over by the Corporation are a mix of residential and commercial properties located in key metro cities. The properties are either for the Corporation’s own use or being held for capital appreciation, which the Corporation will dispose of at an appropriate time and in accordance with directions as stipulated by the regulator.

Accordingly, the Corporation has entered into debt asset swaps wherein the gross carrying amount of the financial and non-financial assets taken over as at March 31, 2021 stood at ` 347 crore and ` 1,432 crore respectively.

Impairment on Financial Instruments - Expected Credit Loss

Under Ind AS, asset classification and provisioning moves from the ‘rule based’, incurred loss model to the Expected Credit Loss (ECL) model of providing for expected future credit losses. Thus, loan loss provisions are made on the basis of the Corporation’s historical loss experience and future expected credit loss, after factoring in various other parameters.

Classification of Assets

| Exposure at Default (EAD) | As at March 31, 2021 |

As at March 31, 2020 |

|---|---|---|

| Stage 1 | 91.4% | 92.2% |

| Stage 2 | 6.3% | 5.5% |

| Stage 3 | 2.3% | 2.3% |

| Total | 100% | 100% |

The increase in the stage 2 accounts is of account of certain assets which were classified as stage 1 in the previous year, but have opted for either ECLGS or OTR and thus have been reclassified as stage 2 based on a qualitative assessment of the respective exposures.

Expected Credit Loss Based on Exposure at Default

(` crore)

| EAD | Individual | Non-Individual | Total | |||

|---|---|---|---|---|---|---|

| Stage 1 | 3,55,367 | 97% | 98,662 | 75% | 4,54,029 | 92% |

| Stage 2 | 7,180 | 2% | 24,367 | 19% | 31,547 | 6% |

| Stage 3 | 4,236 | 1% | 7,396 | 6% | 11,632 | 2% |

| EAD Total | 3,66,783 | 100% | 1,30,425 | 100% | 4,97,208 | 100% |

| ECL | Individual | Non-Individual | Total | |||

|---|---|---|---|---|---|---|

| Stage 1 | 638 | 27% | 449 | 4% | 1,087 | 8% |

| Stage 2 | 802 | 34% | 5,079 | 48% | 5,881 | 45% |

| Stage 3 | 939 | 39% | 5,118 | 48% | 6,057 | 47% |

| ECL Total | 2,379 | 100% | 10,646 | 100% | 13,025 | 100% |

| ECL / EAD | Individual | Non-Individual | Total |

|---|---|---|---|

| Stage 1 | 0.2% | 0.5% | 0.2% |

| Stage 2 | 11.2% | 20.8% | 18.6% |

| Stage 3 | 22.1% | 69.2% | 52.1% |

| ECL / EAD | 0.65% | 8.16% | 2.62% |

The total balance in the Impairment on Financial Instruments – Expected Credit Loss (provisions carried) as at March 31, 2021 amounted to ` 13,025 crore. This is equivalent to 2.62% of the EAD. The balance in the Impairment on Financial Instruments – Expected Credit Loss more than adequately covers loans where the instalments were in arrears for over 90 days.

Fixed Assets and Investment Properties

Net fixed assets as at March 31, 2021 amounted to ` 986 crore. Net additions to fixed assets during the year was ` 105 crore, including rightof- use assets of ` 55 crore.

Net investment in properties as at March 31, 2021 amounted to ` 841 crore. Net additions to investment properties during the year was ` 60 crore.

Resource Mobilisation

Issue of Securities on Qualified Institutions Placement Basis

The Corporation completed its Qualified Institutions Placement (QIP) of equity shares and secured, redeemable non-conver t i b l e debentures simultaneously with warrants in August 2020. The QIP was in accordance with applicable provisions of the Companies Act, 2013, rules framed thereunder and the Securities and Exchange Board of India (Issue of Capital and Disclosure Requirements) Regulations, 2018.

Equity and Warrants

Under the QIP, the Corporation raised ` 10,000 crore through the issue and allotment of 5,68,18,181 equity shares of face value of ` 2 each at an issue price of ` 1,760 per equity share (including a premium of ` 1,758 per equity share).

The Corporation also raised ` 307 crore through the issue and allotment of 1,70,57,400 warrants at an issue price of ` 180 per warrant which was paid upfront. The warrants carry a right exercisable by the warrant holder to exchange each warrant for one equity share of face value of ` 2 each of the Corporation at any time on or before August 10, 2023, at a warrant exercise price of ` 2,165 per equity share, to be paid by the warrant holder at the time of exchange of the warrants. As at March 31, 2021, no warrants had been converted into equity shares.

The maximum equity dilution on account of the aforesaid QIP issue, assuming full conversion of all the warrants into equity shares at the warrant exercise price is 4.23%, based on the enhanced share capital.

Non-Convertible Debentures (NCDs)

Further, the Corporation raised ` 3,693 crore through the issue and allotment of 36,930 secured, redeemable NCDs at par having a tenor of 3 years, carrying a coupon rate of 5.40% payable annually. The NCDs are rated by CRISIL Ratings Limited (CRISIL) and ICRA Limited (ICRA) and are assigned the highest rating ‘CRISIL AAA Stable’ and ‘ICRA AAA/Stable’ respectively.

The equity shares, warrants and NCDs are listed on BSE Limited (BSE) and National Stock Exchange of India Limited (NSE).

Share Capital

As on April 1, 2020, the Corporation had a balance of ` 346 crore in the share capital account. The Corporation has allotted 5,68,18,181 equity shares of ` 2 each pursuant to the QIP issue and 1,50,77,063 shares pursuant to the exercise of stock options by certain employees/ directors. After considering the above allotments during the year, the balance in the share capital account as on March 31, 2021 is ` 361 crore.

Subordinated Debt

As at March 31, 2021, the Corporation’s outstanding subordinated debt stood at ` 4,000 crore. The debt is subordinated to present and future senior indebtedness of the Corporation and has been assigned the highest rating of ‘CRISIL AAA/Stable’ and ‘ICRA AAA/Stable’. The Corporation did not issue any subordinated debt during the year.

Based on the balance term to maturity, as at March 31, 2021, ` 1,800 crore of the book value of subordinated debt was considered as Tier II under the regulatory guidelines for the purpose of capital adequacy computation.

Borrowings

Borrowings as at March 31, 2021 amounted to ` 4,41,365 crore as against ` 4,19,102 crore in the previous year. Borrowings constituted 78% of funds employed as at March 31, 2021. Of the total borrowings, debentures and securities constituted 42%, deposits 34% and term loans 24%.

Summary of Total Borrowings

| Borrowings | March 31, 2021 |

March 31, 2020 |

|---|---|---|

| Term Loans | 1,05,179 | 1,04,909 |

| Market Borrowings | 1,86,055 | 1,81,869 |

| Deposits | 1,50,131 | 1,32,324 |

| Total | 4,41,365 | 4,19,102 |

Non-Convertible Debentures & Commercial Paper

During the year under review, the Corporation raised an amount of ` 49,843 crore through secured redeemable non-conver t i b l e debentures (NCDs), issued in various tranches on a private placement basis, including ` 3,693 crore issued through the QIP.

The Corporation’s NCD issues have been listed on the wholesale debt market segment of the NSE and the BSE. The NCDs have been assigned the highest ratings of ‘CRISIL AAA/ Stable’ and ‘ICRA AAA/Stable’. The Corporation has been regular in making payments of principal and interest on the NCDs.

There are no NCDs which have not been claimed by investors or not paid by the Corporation after the date on which the NCDs became due for redemption.

The Corporation has been qualified as a ‘large corporate’ by SEBI and accordingly has ensured that more than 25% of its incremental borrowings during the year was by way of issuance of debt securities.

The Corporation’s short-term debt programme has been assigned the highest ratings of ‘CRISIL A1+’, ‘ICRA A1+’ and ‘CARE A1+’ by CRISIL, ICRA and CARE Ratings respectively.

As at March 31, 2021, the Corporation had commercial paper (CPs) with an outstanding amount of ` 30,776 crore and the weighted average outstanding maturity was 254 days. CPs constituted 7% of the outstanding borrowing as at March 31, 2021. The CPs of the Corporation are listed on the wholesale debt market segments of the NSE and BSE.

Rupee Denominated Bonds Overseas

Under the Corporation’s Medium Term Note Programme, the Corporation did not raise any funds through Rupee denominated bonds during the year. As at March 31, 2021, total outstanding Rupee denominated bonds overseas stood at ` 2,800 crore.

Deposits

According to regulatory directions, housing finance companies can accept public deposits not exceeding 3 times its net owned funds.

As at March 31, 2021, total outstanding deposits stood at ` 1,50,131 crore compared to ` 1,32,324 crore in the previous year. The number of deposit accounts stood at approximately 21 lac.

CRISIL and ICRA have for the twentysixth consecutive year, reaffirmed their ‘FAAA/Stable’ and ‘MAAA/ Stable’ ratings respectively for HDFC’s deposits. These ratings represent the highest degree of safety regarding timely servicing of financial obligations and also carries the lowest credit risk.

Increasing uncertainties in market conditions led to a flight to safety, which was reflected in the strong mobilisation of deposits of the Corporation during the financial year. The renewal ratio of retail deposits stood at 65% during the year.

The Corporation has over 23,000 active key deposit agents. Brokerage is paid on the deposits generated by deposits agents, depending on the product, amount and period of the deposit. Incentive is also paid on certain products, depending on the amount of deposits generated by the deposit agent. Brokerage and incentive payments are amortised over the period of the deposit.

The Corporation’s online deposit platform continued to be well received and appreciated for its simplicity and convenience, besides being a green initiative. During the year, more than 52% of transactions were through the online deposits. Time and effort was also spent in training key partners to effectively use the online deposit platform. Various other digitalisation initiatives are underway to increase online deposit penetration.

Term Loans from Banks, Institutions and Refinance from National Housing Bank (NHB)

As at March 31, 2021, the total loans outstanding from banks, institutions and NHB (including foreign currency borrowings from domestic banks) amounted to ` 1,05,179 crore as compared to ` 1,04,909 crore as at March 31, 2020.

HDFC’s long-term and short-term bank loan facilities have been assigned the highest rating by CARE and ICRA, signifying highest safety for timely servicing of debt obligations.

During the year, the Corporation availed refinance from NHB under various refinance schemes such as Additional Special Refinancing Facility, Affordable Housing Fund and Regular Refinance Scheme and Promoting Green Housing Refinance Scheme amounting to ` 5,175 crore.

External Commercial Borrowings

The Corporation has in place a medium term note programme for an amount of up to USD 2.8 billion which enables the Corporation to issue rupee/ foreign currency denominated bonds in the international capital markets, subject to regulatory approvals.

During the financial year, the Corporation has not raised any new ECBs.

The outstanding external commercial borrowings (ECBs) constitute borrowings from Asian Development Bank under the Housing Finance Facility Project (USD 12 million) and ECBs under RBI’s Low Cost Affordable Housing Scheme (USD 1,804 million).

Risk Management

The Corporation has a risk management framework with overall governance and oversight by the Risk Management Committee, the Audit and Governance Committee and the Board of Directors. The Corporation recognises that risk management entails a combination of both, a bottom-up and a larger strategic overview of all functions across the organisation. Some of the risk scenarios identified during the year are given below:

Financial Risk Management

The Corporation manages its liquidity, foreign exchange, interest rate and counterparty risks in accordance with its Financial Risk Management and Asset Liability Management Policy and prescribed guidelines.

The Corporation maintains minimum daily liquidity equivalent of at least one month’s market maturities, in the form of units of mutual funds and investment in government securities.

Further, under RBI’s guidelines on Liquidity Risk Management Framework. HFCs would also need to maintain HQLA covering at least the next 30 days of net cash outflows (as defined by the guidelines) with effect from December 2021.

Assets and liabilities in foreign currencies are converted at the rates of exchange prevailing at the year-end. Foreign currency liabilities aggregated to USD 1,856 million as at March 31, 2021. The currency risk on the borrowings is hedged through derivatives such as swaps and options entered into with banks/ financial institutions. As at March 31, 2021, the Corporation’s foreign currency exposure on borrowings net of risk management arrangements was nil, the same as in the previous year.

HDFC’s foreign currency borrowings are linked to USD LIBOR or JPY LIBOR, the risk on which is hedged through coupon only and foreign currency interest rate swaps. The unhedged exposure on the foreign currency coupon for maturities beyond one year is nil on USD and JPY 569 million.

The Corporation enters into INR interest rate swaps to manage the risk arising from the mismatch on account of floating rate loans forming bulk of the assets, and fixed rate borrowings forming a large portion of liabilities. As at March 31, 2021, the Corporation entered into such swaps, converting its fixed rate rupee NCDs of a notional amount of ` 93,160 crore for varying maturities into floating rate liabilities linked to MIBOR. As a result of the swaps, HDFC pays the floating rate and receives the fixed rate.

As at March 31, 2021, 85% of the total assets and 78% of the total liabilities were on a floating rate basis.

The Corporation has an ongoing exercise to hedge potential credit risks on receivables from banks on account of derivative contracts, by entering into collateralisation arrangements with them.

The Corporation does not have any exposures to commodities and hence does not have any commodity price risk.

Asset Liability Management (ALM)

Assets and liabilities are classified on the basis of their contracted maturities. However, the estimates based on past trends in respect of prepayment of loans and renewal of liabilities which are in accordance with the ALM guidelines issued by the regulator have not been taken into consideration while classifying the assets and liabilities under the Schedule III to the Companies Act, 2013.

The ALM position of the Corporation is based on the maturity buckets as per the regulatory guidelines. In computing the information, certain estimates, assumptions and adjustments have been made by the management. The ALM position is as under:

As at March 31, 2021, assets and liabilities with maturity up to 1 year amounted to ` 1,26,346 crore and ` 1,13,241 crore respectively. Assets and liabilities with maturity of greater than 1 year and up to 5 years amounted to ` 2,70,522 crore and ` 2,44,329 crore respectively and assets and liabilities with maturity beyond 5 years amounted to ` 1,83,734 crore and ` 2,23,032 crore respectively.

Capital Adequacy Ratio

The Corporation’s capital adequacy ratio (CAR) stood at 22.2%, of which Tier I capital was 21.5% and Tier II capital was 0.7%. The minimum CAR as per the prescribed regulations is 14% and minimum Tier 1 Capital is 10%.

On or before March 31, 2022, NBFCHFCs are required to maintain a minimum CAR of 15% and minimum Tier 1 Capital at 10%.

As at March 31, 2021, the risk weighted assets stood at around ` 3,98,000 crore.

Internal Control Systems and their Adequacy

The Corporation has instituted adequate internal control systems commensurate with the nature of its business and the size of its operations. Internal audit is carried out by independent firms of chartered accountants and cover all the branches and key areas of business. All significant audit observations and follow-up actions thereon are reported to the Audit and Governance Committee. All the members of the Audit and Governance Committee are independent directors.

Material Developments in Human Resources

The Corporation has always believed that its employees are its most valued resource and has always ensured their all-round development. The employees are trained in functional and behavioural skills to ensure high standards of service to internal and external stakeholders.

During the year, leveraging technology, many of the in-person training programmes were converted into online courses to ensure continuity of knowledge and skill based training during the pandemic. In-house videos on various products and processes were developed by employees to share best practices. Further, the Corporation procured a number of soft skills e-learning courses for its employees.

As at March 31, 2021, the Corporation has 390 offices (excluding offices of HSPL) and the total number of employees is 3,226.

Total assets per employee as at March 31, 2021 stood at ` 171 crore as compared to ` 163 crore in the previous year. The net profit per employee as at March 31, 2021 was ` 3.4 crore compared to ` 3.0 crore in the previous year (after adjusting for sale of strategic investments).

Awards and Recognitions

During the year, some of the awards and recognitions received by the Corporation included:

Subsidiaries and Associates

Though housing finance remains the core business, the Corporation has created tremendous value through its investments in its subsidiary and associate companies and will continue to support these companies whenever required. The Corporation will continue to explore avenues for such investments with the objective of providing a wide range of financial services and products under the HDFC brand name.

During the year, the Corporation’s subsidiary, HDFC ERGO Health Insurance Limited (formerly Apollo Munich Health Insurance Company Limited) was merged into HDFC ERGO. The appointed date of the merger was March 1, 2020 and the effective date was November 13, 2020. Consequently, HDFC ERGO Health Insurance Limited was dissolved with effect from the said date.

RBI had directed the Corporation to reduce its shareholding in its insurance companies to below 50%.

Accordingly, during the year, the Corporation sold 1.43% of its shareholding in HDFC Life for a total consideration of ` 1,398 crore. As at March 31, 2021, the Corporation’s shareholding in HDFC Life stood at 49.97% and ceased to be a subsidiary under the Companies Act, 2013.

However, for the purpose of consolidated financial statements, HDFC Life will continue to be accounted as a subsidiary company. As per IndAS, the Corporation consolidates a subsidiary when it controls the said company.

As per RBI’s directive, the Corporation has to reduce its shareholding in HDFC ERGO to below 50% by May 12, 2021.

During the year, the Corporation made a gross investment of ` 55 crore in its subsidiary, HDFC Sales.

In November 2020, the Corporation entered into an agreement to invest in Renaissance Investment Solutions ARC Private Limited (Renaissance), representing 19.95% of its share capital for a consideration of ` 49.9 lac. Brookfield Property Manager (DIFC) Limited is a majority shareholder in Renaissance. Renaissance will undertake the business of asset reconstruction, subject to receipt of approval from RBI. Renaissance is an associate of the Corporation.

In February 2021, HDFC Property Ventures Limited (HPVL), a wholly owned subsidiary of the Corporation sold its entire stake in Magnum Foundations Pri vate Limited (Magnum). Subsequent to the sale by HPVL, Magnum ceased to be an associate of the Corporation.

In April 2021, the Corporation concluded the sale of its equity stake of 24.48% of the equity capital of Good Host Spaces Private Limited (Good Host) to Baskin Lake Investments Limited. Post the sale, Good Host ceased to be an associate of the Corporation.

The financials with respect to HDFC Bank, HDFC Life and HDFC ERGO are presented as per their statutory financial statements prepared under Indian GAAP.

Review of Key Subsidiary and Associate Companies

HDFC Bank Limited (HDFC Bank)

HDFC and HDFC Bank continue to maintain an arm’s length relationship in accordance with the regulatory framework. Both organisations, however, capitalise on the strong synergies through a system of referrals, special arrangements and cross selling in order to effectively provide a wide range of products and services under the ‘HDFC’ brand name.

As at March 31, 2021, advances of HDFC Bank stood at ` 11,32,837 crore – an increase of 14% over the previous year. Total deposits stood at ` 13,35,060 crore – an increase of 16%. As at March 31, 2021, HDFC Bank’s distribution network includes 5,608 banking outlets and 16,087 ATMs in 2,902 locations.

For the year ended March 31, 2021, HDFC Bank reported a profit after tax of ` 31,117 crore as against ` 26,257 crore in the previous year, representing an increase of 19%.

HDFC together with its wholly owned subsidiaries, HDFC Investments Limited and HDFC Holdings Limited holds 21.1% of the equity share capital of HDFC Bank.

Amid the second wave of COVID-19 in India, HDFC Bank did not declare any dividend for the year ended March 31, 2021, in view of the persisting uncertainty.

HDFC Life Insurance Company Limited (HDFC Life)

As at March 31, 2021, total premium income of HDFC Life stood at ` 38,583 crore as compared to ` 32,707 crore in the previous year, representing a growth of 18%. As at March 31, 2021, the company had a portfolio of 36 individual and 12 group products, along with 7 optional rider benefits, catering to a diverse range of customer needs.

The company continued on its trajectory of delivering consistent and strong business performance in FY21, whilst outpacing industry growth. The company recorded a growth of 17% in terms of individual weighted received premium (WRP) during FY21 as against private industry growth of 8%. The company ranked second in terms of individual weighted received premium, with its private market share increasing from 14.2% to 15.5% in FY21. The private market share within group and overall new business segment stood at 27.6% and 21.5% respectively. This has been delivered on the back of its proven strategy of adhering to a balanced product mix and diversified distribution, whilst leveraging digital capabilities.

Despite logistical challenges through the year, the company insured close to 40 million lives in FY21. The renewal premiums grew by 19% on the back of robust collections in the recently launched long-term savings products, with 13th month persistency improving from 88% in FY20 to 90% in FY21.

HDFC Life has reported a standalone profit after tax of ` 1,360 crore for the year ended March 31, 2021 as against ` 1,295 crore in the previous year.

The new business margin based on actual expenses (post overrun) stood at 26.1% (Previous Year: 25.9%).

As at March 31, 2021, the Indian Embedded Value stood at ` 26,617 crore (Previous Year: ` 20,650 crore). The operating return on embedded value stood at 18.5%.

The solvency ratio of the company was 201% as at March 31, 2021 as against the minimum regulatory requirement of 150%.

HDFC Life recommended a dividend of ` 2.02 per equity share of ` 10 each.

The Corporation’s shareholding in HDFC Life stood at 49.97%.

HDFC Asset Management Company Limited (HDFC AMC)

HDFC AMC is one of India’s largest mutual fund managers. As at March 31, 2021, the quarterly average assets under management (QAAUM) stood at ` 4.2 lac crore compared to ` 3.7 lac crore as at March 31, 2020.

The ratio of equity oriented AUM and non-equity oriented AUM was 43:57. HDFC AMC is the largest actively managed equity-oriented mutual fund in the country with market share at 13.3% in terms of actively managed equity-oriented QAAUM as at March 31, 2021.

For the year ended March 31, 2021, the profit after tax stood at ` 1,326 crore as against ` 1,262 crore in the previous year.

HDFC AMC recommended a final dividend of ` 34 per equity share of ` 5 each compared to the total dividend of ` 28 per share paid in the previous year.

During the year, the Corporation received dividend of ` 314 crore from HDFC AMC.

HDFC holds 52.7% of the equity share capital of HDFC AMC.

HDFC ERGO General Insurance Company Limited (HDFC ERGO)

HDFC ERGO continued to retain its market ranking as the third largest private sector player in the general insurance industry. The company had a market share of 10.8% (private sector) and 6.2% (overall) in terms of gross direct premium for the year ended March 31, 2021.

During the year, HDFC ERGO Health Insurance Limited (formerly Apollo Munich Health Insurance Company Limited) merged with and into HDFC ERGO.

The company offers a complete range of insurance products like motor, health, travel, home and personal accident in the retail segment, customised products like property, marine, aviation, cyber security and liability insurance in the corporate segment and crop insurance. The company had a balanced portfolio mix with the retail segment accounting for 62% of the business.

The gross written premium of HDFC ERGO for the year ended March 31, 2021 stood at ` 12,444 crore compared to ` 9,760 crore in the previous year (on a merged basis).

The combined ratio as at March 31, 2021 stood at 103.2%. The solvency ratio of the company was 190% as at March 31, 2021 as against the minimum regulatory requirement of 150%.

For the year ended March 31, 2021, profit after tax stood at ` 592 crore compared to ` 327 crore in the previous year.

HDFC ERGO paid an interim dividend of ` 3 per equity share of face value ` 10 per share during the year. Accordingly, the Corporation received ` 108 crore as dividend from HDFC ERGO.

HDFC holds 50.6% of the equity share capital of HDFC ERGO.

HDFC Property Funds

HDFC Venture Capital Limited &

HDFC Property Ventures Limited

HDFC Venture Capital Limited (HVCL) is investment manager to HDFC Property Fund, a registered venture capital fund with SEBI. All the balance investments of the close-ended fund have been fully exited during the financial year ended March 31, 2021. The fund generated attractive risk adjusted returns for the investors.

HDFC Property Ventures Limited (HPVL) provides investment advisory services to overseas asset management companies (AMCs). Such AMCs in turn manage and advise Indian and offshore private equity funds and investors.

HDFC holds 80.5% of the equity share capital of HVCL (with the balance held by State Bank of India) and 100% of the equity share capital of HPVL.

The Corporation has sponsored two off shore funds – HIREF International LLC (‘HIREF’) and HIREF International Fund II Pte Ltd (‘HIREF II’).

HIREF was launched in 2007 and has a corpus of USD 800 million and includes USD 50 million of commitment by the Corporation. The fund has made several profitable exits and is in the process of exiting the balance investments. The fund had made 14 investments in total and 5 investments are yet to be exited.

HIREF II had its final closing in April 2015 with a total corpus of USD 321 million which includes USD 40 million of commitment by the Corporation. The Fund has made 10 investments of which 3 investments have been profitably exited.

HDFC Ventures Trustee Company Limited has entered into a trust deed to act as a trustee to ‘HDFC India Real Estate Fund III’ (‘HIREF III’) which is registered under SEBI (Alternative Investment Funds) Regulations, 2012. HIREF III is in the process of raising INR equivalent of USD 500 million. HIREF III has received a commitment from a marque global investor.

HDFC Capital Advisors Limited

HDFC Capital Advisors Limited (HDFC Capital) is in the business of providing investment management services for real estate private equity financing. The Company also seeks to promote innovation and the adoption of new technologies within the real estate sector by investing in and partnering with technology companies.

HDFC Capital is one of the largest residential real estate fund managers in India with funds under management in excess of USD 1.3 billion. The company is the investment manager to HDFC Capital Affordable Real Estate Fund 1 (H-CARE 1) and HDFC Capital Affordable Real Estate Fund 2 (H-CARE 2), which are registered with SEBI as Category II Alternative Investment Funds. In addition, the company is also an investment advisor to a special situations fund focused on high-yield opportunities in the Indian residential real estate sector.

HDFC Capital was set up with the primary objective of providing longterm equity and mezzanine capital to developers at the land and preapproval stage for the development of affordable and mid-income housing in India. H-CARE 1 and H-CARE 2 combine to create a USD 1.1 billion platform targeting the development of affordable and mid-income housing. These funds are committed with leading developers across India in the affordable and mid-income housing space. The platform is expected to support the development of approximately 75 residential projects and 1.7 lac residential units in urban India.

HDFC Capital believes that new technologies will play a vital role in the creation of efficiencies within the real estate development cycle which is critical for affordable housing projects. The company has set up the HDFC Affordable Real Estate and Technology Programme (H@ ART), a first-of-its-kind initiative aimed at creating efficiencies and lowering costs in each part of the development cycle for a real estate project. H@ART seeks to invest, partner and mentor real estate technology companies that drive innovation and efficiencies within the affordable housing ecosystem.

HDFC Capital is a wholly owned subsidiary of the Corporation.

HDFC Sales Private Limited (HSPL)

HSPL continues to strengthen the Corporation’s marketing and sales efforts by providing a dedicated sales force to sell home loans and other financial products.

HSPL has a presence in 203 locations. During the year under review, HSPL sourced loans accounting for 54% of individual loans disbursed by HDFC.

During the year, the company made a profit of ` 19 crore.

HSPL is a wholly owned subsidiary of the Corporation.

HDFC Credila Financial Services Limited (HDFC Credila)

HDFC Credila is India’s first dedicated education loan company, providing loans to students pursuing higher education in India and abroad. As at March 31, 2021, HDFC Credila had cumulatively disbursed ` 12,055 crore to over 70,922 customers. The outstanding loan book stood at ` 6,267 crore. The average loan amount approved during the year was ` 26.8 lac.

For the year ended March 31, 2021, HDFC Credila reported a profit after tax of ` 155 crore as against ` 123 crore in the previous year, representing a growth of 26%.

As at March 31, 2021, the capital adequacy ratio stood at 24% and Tier 1 capital stood at 17.7%.

In addition to having its own sales team, branch network and digital channels for sourcing applications, HDFC Credila capitalises on HDFC Group’s distribution network to source and market education loans.

HDFC Credila’s borrowers are entitled to income tax exemption under Section 80E of the Income Tax Act, 1961.

HDFC Credila is a wholly owned subsidiary of the Corporation.

HDFC Education and Development Services Private Limited (HDFC Edu)

HDFC Edu is the Corporation’s wholly owned subsidiary which focuses on the education sector.

The objective of HDFC Edu entering the education space is to imbibe best practices in education and facilitate innovation, thereby creating a visible impact on the educations system in the country.

The company provides services to The HDFC Schools which are located in Gurugram, Pune and Bengaluru. These schools follow the National Curriculum Framework, 2005 and are affiliated with the Central Board of Secondary Education.

The HDFC Schools believe in inclusive education and cater to children with special needs with trained teachers to take care of them. The schools also have children from underprivileged backgrounds. The schools now have more than 2,500 students and have created employment for more than 500 people.

With the help of the technology support provided by the Company, all three schools to which we provide services were quick to adapt to the COVID-19 situation. Even though the schools are locked up physically, online interactive classes had commenced via virtual classrooms almost immediately. The Company is continuously monitoring the situations advising the schools to follow the various Government directives of different states.

AUDITED CONSOLIDATED ACCOUNTS

Whilst Ind AS has been made applicable for NBFCs, including housing finance companies from the accounting period beginning April 1, 2018, the same is still pending for adoption by banks and insurance companies.

The consolidated financial statements comprise the standalone financial statements of the Corporation together with its subsidiaries which are consolidated on a line-by-line basis and its associates which are accounted on the equity method.

On a consolidated basis for the year ended March 31, 2021, the profit before tax was ` 24,237 crore as compared to ` 26,193 crore in the previous year.

The total comprehensive income stood at ` 22,069 crore as compared to ` 16,613 crore in the previous year.

The profit attributable to the Corporation during the year ended March 31, 2021 was ` 18,740 crore.

The post-tax return on assets for the consolidated group accounts for the year ended March 31, 2021 was 2.6%. The return on equity stood at 13.7%. The basic and diluted earnings per share (on a face value of ` 2 per share) for the group was ` 105.6 and ` 104.7 respectively.